Law firm partner billing rates across the AmLaw market continue to rise, but beneath those increases lies a more nuanced pricing landscape that corporate legal departments must navigate strategically.

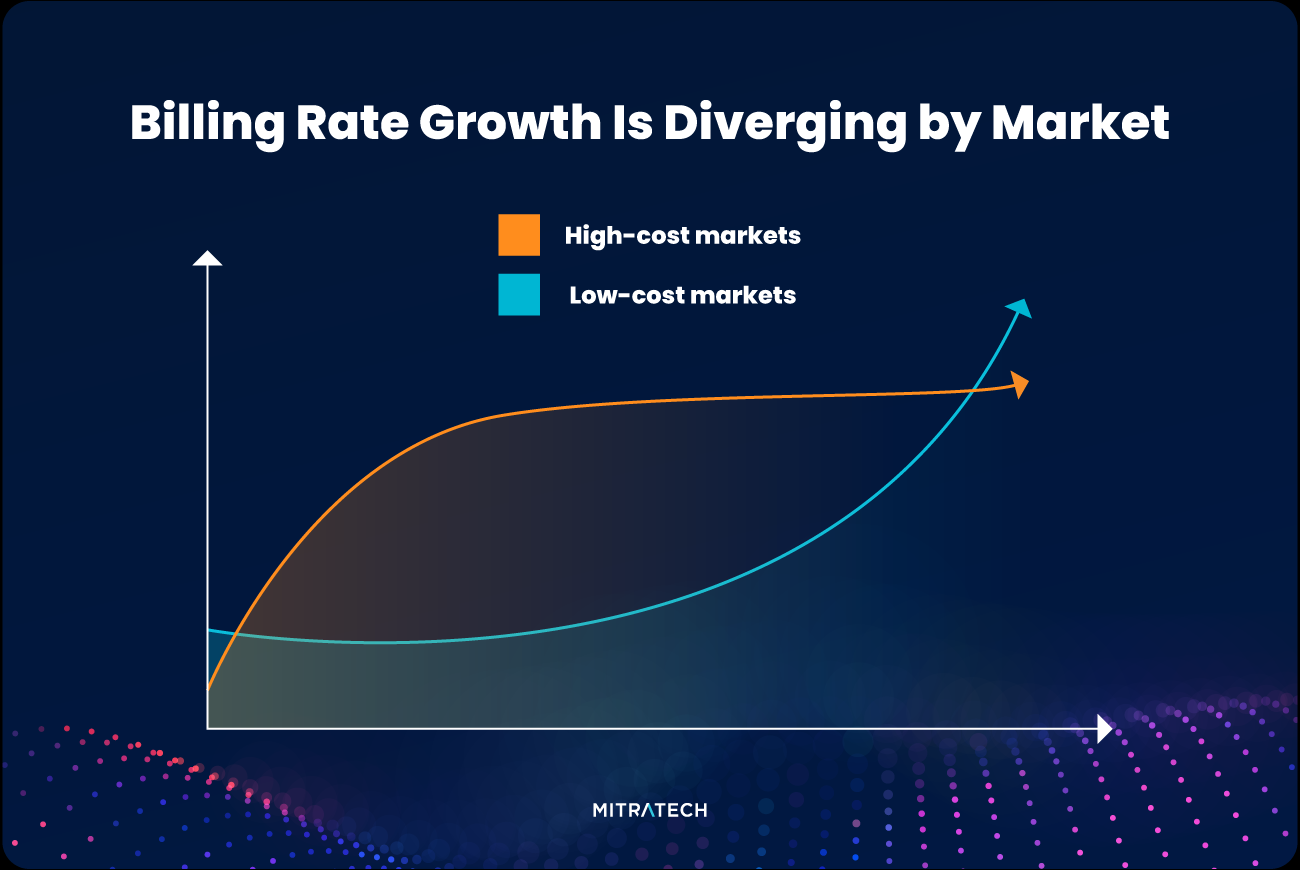

From 2023 to 2025, rate behavior across high‑ and low‑cost markets shows a clear pattern: high‑cost markets are stabilizing (after years of aggressive double-digit growth) while low‑cost markets are accelerating.

For corporate legal departments, this matters. Not just in budget planning, but in how they structure negotiations, push back on rate proposals, and assess value across a firm’s office footprint.

Key Billing Rate Trends for 2026 at a Glance:

- Partner billing rates are still rising, but unevenly

- High-cost markets (NY, SF, DC) are stabilizing

- Lower-cost markets are seeing faster rate increases

- Negotiation leverage is becoming more location-specific

- Data-driven benchmarking is increasingly critical

Below are the trends* that stand out, and what they should mean for your 2026 rate discussions.

In this Article:

1. High‑Cost Markets Are Approaching a Ceiling

In major markets such as New York, San Francisco, and Washington, partner billing rate growth is slowing or even declining in some AmLaw tiers. Several high‑cost segments show:

- Pullbacks or softening after aggressive 2024 increases

- Consecutive declines in 2024/25 (particularly in the AMLAW 51–100 tier)

- A return to more modest year‑over‑year billing rate changes

Why it matters for legal departments: This environment gives corporate legal teams more negotiating leverage. Many firms in major metros already pushed rates aggressively last year. That creates an opportunity to:

- Push back on rate increases

- Re-anchor conversations around value

- Challenge assumptions tied to “premium market” pricing

2. Low‑Cost Markets Are Driving the Next Wave of Billing Rate Growth (with Nuance)

While high‑cost markets appear to cool after years of double-digit increases, low‑cost markets saw significant jumps, especially in 2025. The data shows:

- AmLaw 20 low‑cost offices jumping 17–18%

- AmLaw 21–50 low‑cost offices jumping 26%

This shift reflects a realignment: AmLaw 50 firms are expanding into the secondary market (Austin, Denver, Houston, Nashville) and repositioning their lower‑cost offices upward to close historical pricing gaps.

So, where is the value now?

Mid-market firms continue to offer value in the market, but identifying which firms deliver that value is becoming more important than ever.

What This Means for 2026 Rate Negotiations

Billing rate trends are no longer uniform across the market; they are diverging by geography and firm strategy.

What legal departments should do:

- Evaluate billing rates by office location, not just firm brand

- Assess who is doing the work, not just partner rates

- Use benchmarking data to compare firms objectively

- Identify mid-market alternatives in lower-cost regions

In this environment, your leverage is not uniform; it’s targeted. The departments that negotiate based on where the work is done, who is doing it, and how the market is moving will be in the strongest position.

How to Approach Law Firm Rate Negotiations in 2026

To respond effectively to shifting billing rates:

- Benchmark billing rates against peers and market data

- Segment firms by value, not just brand or prestige

- Leverage cooling high-cost markets in negotiations

- Explore alternative fee arrangements (AFAs) where appropriate

If you’re preparing for 2026 rate negotiations and want help benchmarking your firms, or shaping a data‑driven rate strategy, our Outside Counsel Advisory Team would love to walk through these trends and help your team translate them into practical negotiation tactics.

* Trends analyzing 2024 and 2025 spend data across Mitratech’s Managed Bill Review Solution