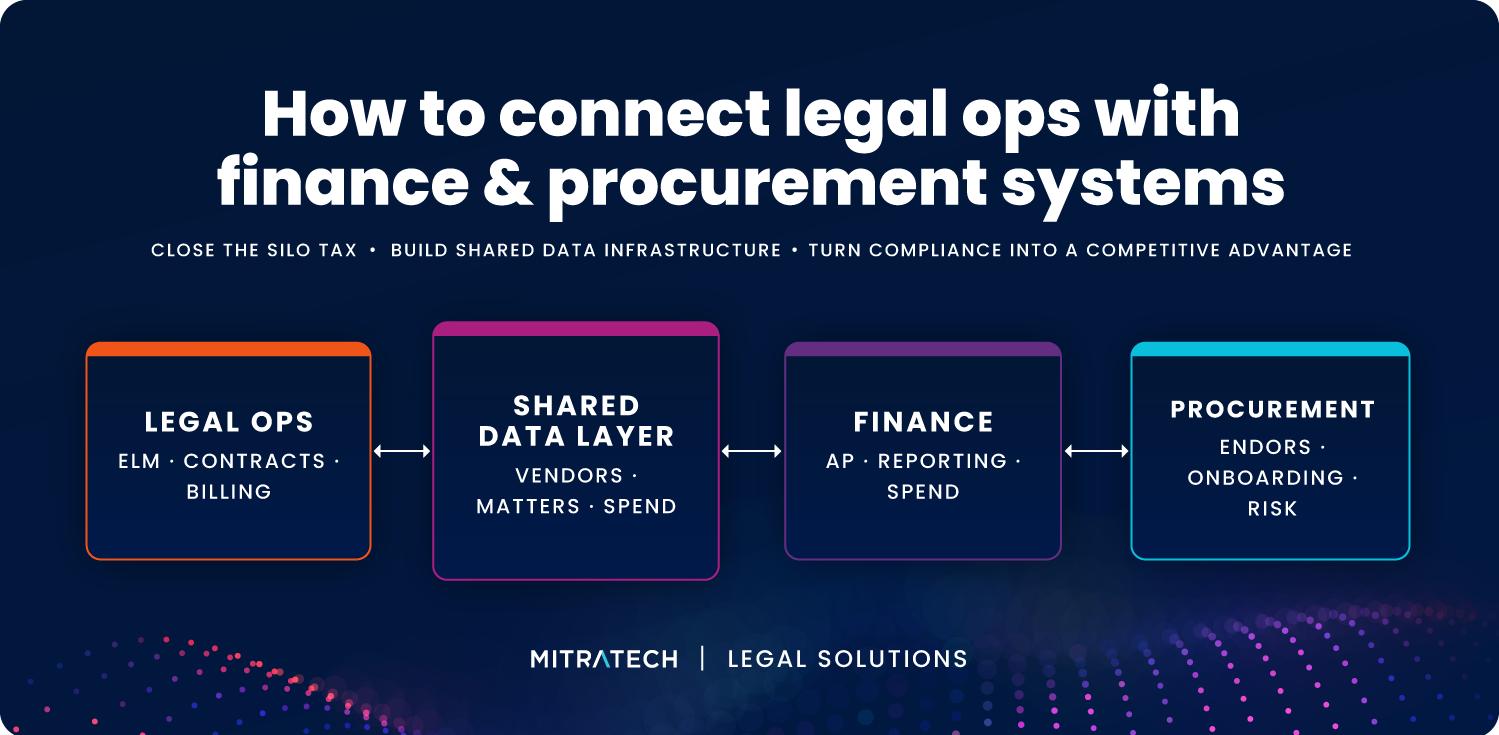

Most legal operations teams don't have a strategy problem. They have a data problem, and it's costing them more than they realize.

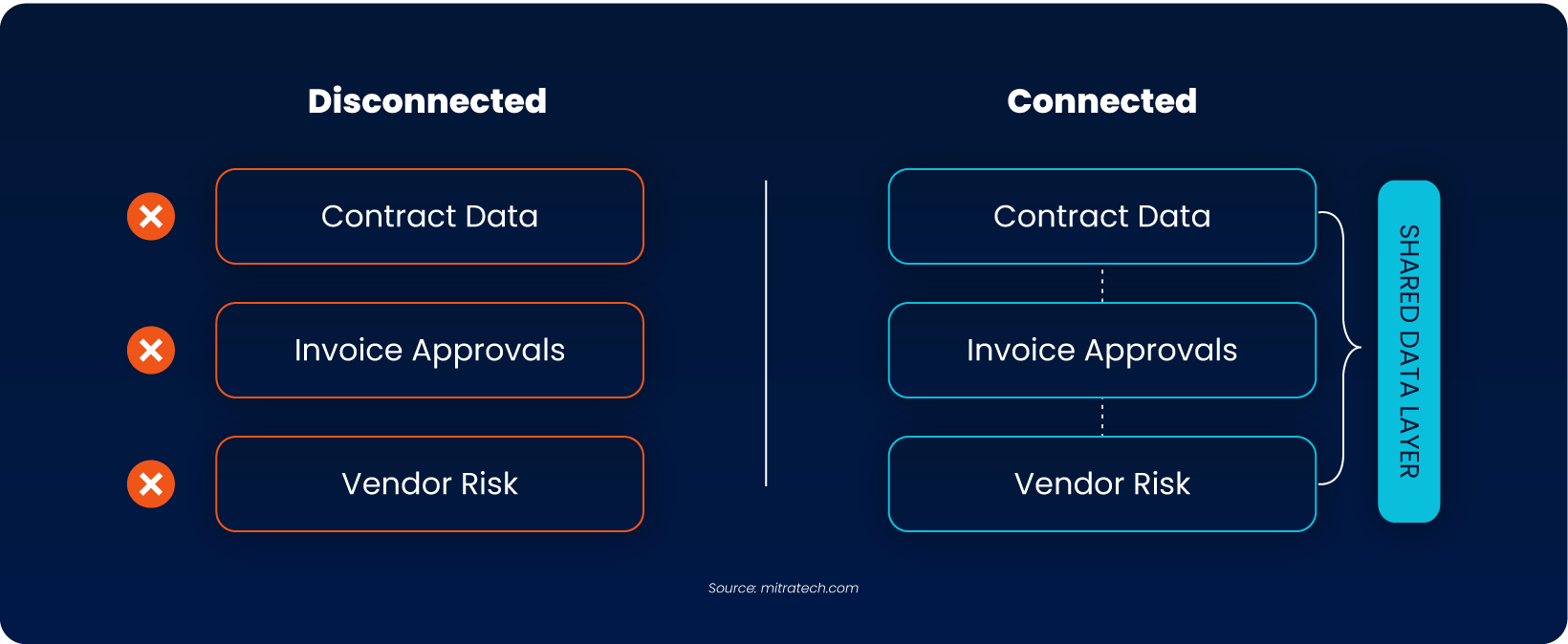

When contract data lives in one system, invoice approvals run through another, and vendor risk assessments happen in a completely separate workflow, you end up paying what practitioners call the ‘silo tax’: the cumulative drag of manual reconciliation, duplicated effort, and the compliance gaps that emerge when no single team has the full picture.

In Part 1 of this series, we covered how to build the organizational relationships with finance and procurement that make integration possible. This guide covers how to close the gap technically: the integrations, data models, controls, and governance frameworks that make legal, finance, and procurement operate from a single version of the truth.

En este artículo:

- How Do You Connect Legal Operations with Finance and Procurement Systems?

- Step 1: Establish a Shared Data Model Before Integration Begins

- Step 2: Build Bidirectional Legal-to-AP Data Flow

- Step 3: Build a Single Vendor Record Across All Three Systems

- Step 4: Embed Controls Directly in Workflows

- Step 5: Govern AI-Assisted Decisions Before Deploying Them

- Implementation Sequence: What to Build First

- The Metrics That Prove Integration Value to Finance and Legal Leadership

- Preguntas frecuentes

How Do You Connect Legal Operations with Finance and Procurement Systems?

The short answer: through a combination of a shared data model, bidirectional invoice-to-AP integration, a unified vendor record, and embedded workflow controls. Each piece depends on the others. The specifics vary by platform, but the architecture is consistent across organizations that have done this well. Here’s how each component works.

Step 1: Establish a Shared Data Model Before Integration Begins

No integration works reliably if the systems on either end use different identifiers, field definitions, or relationship structures for the same real-world concepts. This is the first technical problem to solve, and it’s almost always underestimated in project scoping.

The data mapping questions that must be answered before integration development begins:

- What constitutes a ‘matter,’ and how does it connect to financial cost centers?

- How does a vendor record in the procurement system correspond to outside counsel in the legal e-billing system — same record or linked records?

- How do matter budgets in the legal system map to cost center allocations in the financial management module?

- When an invoice is split across multiple matters, how does that cost allocation persist through the AP process?

- What is the authoritative source for each data type, and what are the synchronization rules when definitions diverge?

For every entity that needs to flow between systems, document how it’s defined in each system, which system is the source of truth, and what happens when values conflict. Systems that share clean, well-defined data can be integrated reliably. Systems that use mismatched terminology for the same concepts will produce reconciliation problems indefinitely, regardless of how good the technical connection is.

In practice, this means a dedicated cross-functional data mapping exercise before any integration development begins. Assign a small working group (like legal ops, finance ops, and a procurement lead) whose explicit job is to define and maintain the shared data model.

Step 2: Build Bidirectional Legal-to-AP Data Flow

The integration between legal invoice processing and accounts payable is where the financial exposure is most immediate. It’s also where integration quality matters most.

The mechanics of this integration vary by platform, but the underlying architecture is consistent: most legal e-billing systems connect to AP through a periodic extract-and-import cycle rather than a live API connection. Understanding how that cycle works is essential for implementation planning, regardless of which platform you’re using.

How the extract-and-import cycle works

- Outbound (legal to AP): The e-billing system generates a periodic extract of approved invoices containing whichever fields you’ve configured. When a legal invoice is approved, it becomes eligible for the next extract run — it doesn’t push to AP automatically.

- Inbound (AP to legal): When AP processes payments, confirmation data returns as an import file that updates the corresponding invoice records with payment amount and date. Without this return flow configured correctly, legal teams reconcile payment status manually against bank statements.

The configuration work that matters most on the outbound side is the logic that determines which invoices are included in each extract. Most platforms allow you to define rules that automatically flag approved invoices as ready for payment processing, eliminating the need for manual updates per record. Getting this rule logic right before go-live is one of the more consequential decisions in the setup; a misconfigured rule can exclude invoices that should be paid or pull in ones that shouldn’t be.

The cost allocation problem that breaks most integrations

When an invoice spans multiple matters or cost centers, that line-item granularity needs to be explicitly included in the extract fields. It won’t carry through automatically. If the allocation fields aren’t mapped into the AP output configuration, cost splits that exist in the e-billing system get collapsed into a single total in the AP extract.

This is consistently where legal-to-AP integrations break down in practice. Avoiding it requires careful field-mapping work, realistic test data covering multi-matter invoices, split cost allocations, credits, and write-downs, and validation of the full import cycle before go-live, not just the extract.

Platform note: In TeamConnect, this integration is handled through a dedicated AP Link module: a separately installed component that requires its own configuration steps before use. The same extract-and-import architecture applies; the setup sequence is specific to the platform.

Step 3: Build a Single Vendor Record Across All Three Systems

Third-party risk is one of the most significant pressure points in the legal-finance-procurement intersection, and disconnected vendor data creates particularly acute exposure.

Consider what happens when a high-risk vendor gets approved through procurement’s standard onboarding without triggering a legal review. Or when outside counsel billing rates and performance history aren’t visible to the team, making future panel assignment decisions. Or when a vendor relationship spanning multiple business units isn’t visible in aggregate anywhere in the organization.

Integrated vendor oversight requires that procurement data, contract data, and invoice data all point to the same vendor record.

Architecture for a unified vendor record

One authoritative system. Either the procurement system or a dedicated vendor management platform holds the master vendor record: legal name, tax identifier, banking information, screening status, approval history. All other systems reference this record.

Outside counsel records linked to the master. Law firm records in the e-billing system must be mapped to corresponding vendor records in procurement. This mapping allows billing anomalies to be identified across a firm’s full book of work, not just invoice by invoice.

Bidirectional sync for panel changes. When a firm is added to or removed from the approved panel, that change syncs automatically between the legal system and the procurement vendor database. Manual updates on multiple sides create conditions for a deactivated firm to continue receiving work because one system wasn’t updated.

Aggregate risk visibility across business units. A vendor serving multiple business units should show consolidated risk indicators from all relationships. A vendor that appears low-risk in any single engagement may look materially different when invoice patterns and contract terms are consolidated.

Budget collaboration with outside counsel via structured requests

Beyond tracking spend internally, mature legal-finance integrations extend budget visibility to outside counsel directly. The pattern: outside counsel receive formal budget requests for specific matters, respond with estimated amounts through a portal or structured channel, and bill against approved figures that create a documented, auditable record of what was estimated, approved, and ultimately billed.

The operational details vary by platform, but the principle is consistent: budget requests should be generated as close to automatically as possible (triggered by matter and account activation), and the e-billing system should always be the system of record when values appear inconsistent between systems. Adjustments made internally after a request has been sent to outside counsel don’t automatically reflect on their end; a new sync or updated request is required.

Step 4: Embed Controls Directly in Workflows

The most effective compliance controls are the ones that can’t be bypassed because they’re embedded in the workflow itself. A billing guideline check that’s a separate manual step will be skipped under time pressure. An automatic gate runs every time.

Billing guideline enforcement at invoice submission

Before an invoice reaches a human reviewer, the system automatically checks it against the billing guidelines in the engagement letter: are the rates within the agreed range, are billing increments compliant, are there line items for activities the guidelines prohibit? Non-compliant line items get flagged before the invoice enters the review queue. The reviewer sees a pre-screened invoice with specific exceptions already identified, not a full document they’d need to cross-reference manually against engagement terms.

Budget threshold alerts before spend is committed

When matter-level budget data in the legal system connects to commitment tracking in finance, it becomes possible to alert matter managers before spend thresholds are crossed rather than after. A 75% budget utilization alert gives the matter team time to have a meaningful conversation with outside counsel about remaining scope. An alert that fires only after the budget is exceeded is documentation of a problem that’s now harder to fix.

The most useful budget dashboards show two figures that often diverge: what’s been spent against fully approved invoices, and what the spend picture looks like if all in-process invoices were approved. That second figure is the one that prevents surprises. For organizations with outside counsel across multiple jurisdictions, currency normalization — using the exchange rate captured at the time of invoice posting — matters for accurate cross-border budget tracking.

The underlying budget account structure matters too. When budget accounts are organized by vendor and phase/task code at the time of matter creation (not configured separately after the fact) budget variance can be sliced by vendor, by phase and task code, by fiscal period, or viewed in aggregate without additional setup.

Vendor activation gates in procurement

When a new supplier is being onboarded, the procurement workflow should require completion of legal review before the vendor can be activated in the system. This isn’t a notification; it’s a hard gate. The vendor record stays inactive until legal review is confirmed complete, which prevents the scenario where operational urgency drives procurement teams to activate vendors before due diligence is done.

Contract term flags for approaching key dates

Renewal windows, rate escalation trigger dates, termination notice deadlines: these are the dates that create financial exposure when they’re missed. When contract data is centralized and connected to a monitoring system, approaching key dates surface automatically to the right person with enough lead time to act.

Step 5: Govern AI-Assisted Decisions Before Deploying Them

AI tools are proliferating across legal, finance, and procurement. AI-assisted invoice processing can dramatically reduce routine review time — catching duplicate submissions, flagging billing guideline violations, and surfacing the small percentage of invoices that genuinely need human attention. But AI-assisted decisions in regulated workflows create an auditability obligation that most organizations aren’t yet taking seriously enough.

When an AI tool flags an invoice as non-compliant, that determination needs to be traceable: which rule triggered it, what data it was based on, and what the human reviewer did with the recommendation. Organizations deploying AI in these workflows without a governance framework are creating a new category of compliance exposure while trying to reduce an existing one.

Required governance infrastructure

Audit trail for AI-assisted decisions. Every AI flag or recommendation that results in a human decision needs a record: what the AI identified, what confidence level it assigned, what action the reviewer took, and the timestamp for each step.

Model validation and refresh cycles. AI tools trained on historical billing data drift as outside counsel practices change, rate structures evolve, and billing guidelines are updated. Without a defined validation cadence, model accuracy degrades silently. Define who owns the model, who validates it, and how often.

Explainability standards. For consequential decisions — payment holds, vendor deactivation, billing dispute initiation — the AI tool needs to produce a human-readable explanation of its determination. Reviewers who don’t understand why something was flagged can’t make a sound judgment about what to do with it.

Clear escalation paths for AI errors. When an AI tool produces a false positive or misses a genuine exception, there needs to be a defined process for identifying the error, correcting the immediate decision, and updating the model or its configurations. Without this, AI errors recur and compound.

Treat AI governance as an extension of existing compliance infrastructure: same audit trail requirements, same documentation standards, same escalation paths. The AI tools that deliver sustainable value are the ones designed to operate within that framework.

Implementation Sequence: What to Build First

For organizations beginning to connect legal operations with finance and procurement systems, the path forward is systematic progress on high-leverage problems — not a grand platform transformation.

| Fase | Enfoque | Primary Outcome |

|---|---|---|

| 1 | Invoice-to-payment workflow | Eliminate manual reconciliation; billing guideline enforcement at invoice submission |

| 2 | Vendor data model | Single authoritative vendor record across procurement, legal, and finance; automated panel sync |

| 3 | High-value controls | Budget threshold alerts; contract date flags; vendor activation gates requiring legal review |

| 4 | Shared reporting | Common spend/risk/performance view for finance and legal without manual exports |

| 5 | AI assistance | Automated invoice review, spend pattern analysis, anomaly detection — built on clean data from phases 1–4 |

Note on Phase 5: AI tools perform best on top of clean, consistent data. Deploying AI-assisted capabilities before the foundational integrations are in place creates data quality problems that undermine AI performance and complicate the governance obligations described above.

The Metrics That Prove Integration Value to Finance and Legal Leadership

When legal and finance share a common data model and reporting infrastructure, legal ops can speak directly to metrics that matter at the executive level rather than abstract legal metrics but business performance indicators that CFOs evaluate alongside other operational data:

- Outside counsel spend as a percentage of revenue

- Budget variance by matter type (requires reconciled legal matter budgets and finance cost center data)

- Índice de excepciones en las facturas por bufete de abogados externo (solo visible cuando los datos de las directrices de facturación y los datos de las facturas están vinculados)

- Contract cycle time by business unit

- Incidentes de riesgo relacionados con los proveedores según la vía de incorporación (muestra si la revisión jurídica en el proceso de incorporación guarda relación con la reducción del riesgo en fases posteriores)

- Compliance incident rate and trend over time

Legal operations functions that can report on these metrics are increasingly involved in strategic planning conversations — not just as compliance checkpoints, but as sources of operational intelligence. That’s what integration ultimately enables: not just fewer manual steps, but a different kind of organizational standing for legal ops.

Preguntas frecuentes

What does ‘bidirectional data flow’ between legal and AP mean in practice?

It means invoice data flows from your e-billing system to AP for payment processing, and payment confirmation data flows back to update invoice records automatically. Most platforms handle this through a configured extract-and-import cycle rather than a live API connection. The key configuration work is ensuring the right fields are included in both directions, particularly cost allocation data on the outbound side, and that rules automate the selection of invoices ready for payment rather than requiring manual updates per record.

How do you enforce contract terms consistently across legal, finance, and procurement?

Consistent enforcement requires contract data to be accessible to every system that needs to act on it. When billing guidelines in an engagement letter are visible to the invoice processing system, violations can be caught automatically before a human reviewer sees the invoice. When payment authorization workflows in finance can verify contract terms before releasing funds, off-contract spend gets intercepted before it happens. This only works when contract data is centralized and connected to downstream operational systems, not stored in a repository that other systems can’t read.

What integration challenges do teams consistently underestimate?

Field-level data mapping is the most common one. A high-level connection between systems is much easier to establish than one that correctly handles cost allocation splits, multi-matter invoices, credits, and write-downs. The edge cases in financial data are where integrations break down, and testing needs to specifically target those scenarios before go-live. Teams also consistently underestimate the organizational work required (like shared data definitions, agreed ownership at handoff points, and governance structures) without which even technically sound integrations fail in use.

How does automation reduce compliance risk?

Automation reduces compliance risk primarily by eliminating the manual steps where errors and inconsistencies occur. When a billing guideline check runs automatically on every invoice, the outcome doesn’t depend on whether a reviewer happened to cross-reference engagement terms before approving. The audit trail is also more reliable: automated controls produce consistent, queryable records of what happened and why — which is what auditors actually need.

What regulatory compliance priorities should legal ops technology address in 2026?

Tax reporting requirements around e-invoicing mandates, anti-money laundering and KYC compliance for vendor onboarding, data privacy obligations affecting vendor data handling, and sector-specific regulations for financial services, healthcare, and government contractors are generating the most compliance activity. More than a third of compliance leaders cite regulatory uncertainty as a top operational concern, which puts a premium on systems that can adapt controls as requirements evolve rather than requiring full reconfiguration.

What structural factors support effective system integration?

Technology is necessary but not sufficient. Successful integration also requires shared ownership of key metrics across departments so the integration has organizational sponsors, not just technical ones; agreed data definitions that prevent systems from using different vocabulary for the same facts; and governance structures that make clear who is responsible when controls fail. The technology makes integration possible. The organizational alignment (covered in Part 1 of this series) makes it sustainable.

See how Mitratech connects legal, finance, and procurement in practice.

TeamConnect gives legal ops teams the integrations, controls, and reporting infrastructure to stop reconciling manually and start operating strategically.

Véalo en acción